By Evan Brandt

July 24, 2019 – Sometimes, shouting into the wilderness gets results.

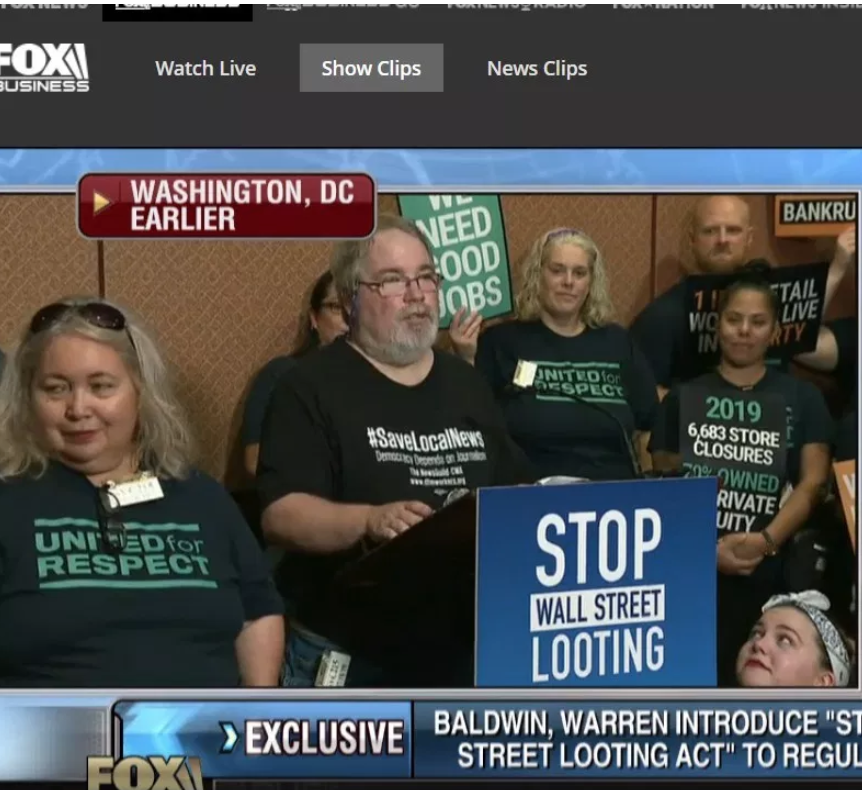

Last week I took a pilgrimage to Washington, D.C. to take part in a press conference announcing the introduction of the “Stop Wall Street Looting Act.”

To be clear, I had not read the proposed legislation and I was not there to endorse it

I was there to speak in the hopes that the introduction of the bill by Massachusetts Senator and Democratic presidential front-runner Elizabeth Warren will help the country to wake up to the threat posed by the ownership of local news by hedge funds that have no intention of keeping the enterprise afloat.

I was invited by The NewsGuild and its parent union, the Communications Workers of America, I suspect, because I won’t shut up about this subject.

It’s about more than saving my job, which admittedly I would be happy to do.

It’s about the importance of local journalism, the accountability it brings to the democratic foundations on which the larger democracy rests.

And it’s about sounding the alarm about what that will do in hundreds of communities across the country, further straining the bonds that bind us together.

A long-time shop steward in the Guild, I have watched journalists, Guild and non-Guild, cut from the staff at The Mercury, or flee when a buyout is offered, to the point that we struggle to cover this community the way it deserves to be covered.

And yes, I understand that newspapers, local and otherwise, not owned by hedge funds are suffering from the same losses, but not at the same pace and not for the same reason.

Some local papers are cutting staff and selling off assets in an attempt to survive.

But as investigative reporter Julie Reynolds has revealed over the course of the past year, Alden Global Capital, the company that owns The Mercury and, most recently, The Reading Eagle, has no interest in our survival; only its own enrichment at our expense.

You can read Reynold’s work here, at the Digital First Media Workers web page, and the picture it reveals is disturbing to say the least.

Here is the best link for a primer on what Reynolds has revealed about the fund;

- Information about the Labor Department investigation of Alden’s investing of employee pensions in its own risky funds;

- Selling newspaper offices and retail chain headquarters to its own subsidiaries and then charging rent to extract profit;

- How Alden uses what profits its newspapers do generate not to invest in the papers or retain their remaining workers, but to gamble on other investments that have nothing to do with the preservation of local news;

- How some of those profits were used to buy co-founder Randall Smith more than a dozen mansions in south Florida. (I mean how many mansions can you live in at one time?)

These and countless other Reynolds revelations show the company’s interest is not in saving local news, not even close, but in feeding off its weakened state to extract the profit that is to be found at the expense of all else.

And that includes Pottstown’s local newspaper, as well as Lansdale’s local newspaper, Norristown’s local newspaper, West Chester’s local newspaper, Delaware County’s local newspaper, Trenton, N.J.’s local newspaper and, now added to the list for a bargain price of a $5 million bankruptcy sale, Reading’s local newspaper.

The metaphor I finally hit upon while part of a team explaining these facts to congressional staffers Thursday was this: Yes, the Internet, Craigslist, Google, Facebook and newspaper management’s failure to adapt quickly to those challenges to its business model have wounded local news.

Some still manage a profit, some break even, so consider local news to be a patient with a pretty serious chronic condition.

Now give that patient flesh-eating bacteria. That’s the additional threat hedge fund ownership poses to the survival of the patient.

And it is the threat I traveled to D.C. to highlight.

I was not the only speaker. In fact, Reynolds was there as well and her comments were similar to her op-ed titled “A Hedge Fund Stripped My Newspaper for Parts” that ran in Newsweek the day she spoke.

“Since I left the Herald in 2015, things have gotten even worse. Friends there tell me deadlines are now 2 p.m. because the paper is copyedited, designed and printed in a ‘hub’ more than five hours away. This means city council votes and even high school sports scores rarely make it into the print edition,” she wrote.

Regular readers of The Mercury and this blog recognize that pattern.

We too are designed and paginated at a “hub.”

Worse yet, I was recently informed that due to the purchase of The Reading Eagle, our scheduled spot on the press (where all Digital First Media’s local PA papers are printed one after the other) was moved back.

To 6 p.m.

As many of you no doubt noticed, when the July 12 print edition of The Mercury hit porches, driveways and newsstands, there was not a whisper of the flood that had caused more than $1 million in damages to Pottstown the afternoon and evening before.

As many of you no doubt noticed, when the July 12 print edition of The Mercury hit porches, driveways and newsstands, there was not a whisper of the flood that had caused more than $1 million in damages to Pottstown the afternoon and evening before.

At 6:15 p.m. that Thursday, I got back from wading thigh-deep into the flood on Walnut Street to take photos and interview shell-shocked residents, only to be informed that all the pages had already been sent.

The next day’s front page featured a centerpiece about a police dog that had cancer. Heartrending no doubt, but certainly not the most important news of the day. The Reading Eagle, which had taken over our spot in the press, did have news of the flood in its print edition the next day.

That night I put together an on-line story with more than 20 photos and video anyway (because after all, we are supposed to be “Digital First” and some coverage was better than no coverage) but that story ran inside, two days later.

This was not a decision that was made by a newspaper company; a company that understands its purpose, its responsibility to inform its community; a company with even a shred of journalistic self-respect. This is a decision that was made by a company that owns newspapers; and shoe stores; and drug stores; and real estate ventures.

That is what hedge fund ownership means to local news and that was what I wanted a national audience to understand. Initially, I was told I would not be speaking, but I found out four hours before the press conference that I would.

Here’s what I said:

My name is Evan Brandt and I have been a reporter for 20 years at The Pottstown Mercury in Pottstown Pennsylvania and I love my job, but its getting harder and harder to do that job with hedge fund ownership of my newspaper.

When I started there were nine reporters in the newsroom and we now have three. We no longer have a newsroom in fact. They closed the building, sold the building and I now work out of an office in my attic.

When I began 20 years ago, I used to cover one community. Now, at election time, I keep an eye on 50. So let’s just say there’s some stuff that goes uncovered, and that’s not the public service that community journalism is supposed to be.

Community journalism is where democracy begins; accountability that begins on the local level. The public official who doesn’t pay his taxes and is exposed in the local newspaper, or the local web site, usually does not go on to become a county commissioner, a state senator of a Congressman.

All of the people who make the rules of democracy, with one notable exception, begin as local elected officials, and they grow up with this idea of accountability as they move on in their careers and when they get to Washington, they understand how the process works.

That process is breaking down at the lower level, and is becoming invisible.

It’s important to note that there are newspaper companies, and there are companies that own newspapers. Hedge funds are the latter. They don’t care about the content. They don’t care about the communities where their newspaper are located. And they don’t care about the people who work there.

They are there for profit. Period.

And they will get that profit at any price. All too often it is the communities and the newspaper workers who pay that price, through lay-offs, through selling off newspaper offices and assets and disconnected communities, which is something Julie addressed so well.

Now more than ever, Americans need to strengthen the bonds that bring us together in our common cause, not weaken them.

Wall Street exists to pursue profit. That’s its purpose.

But maybe it’s time to recognize that some institutions in America are more important than profit; that these institutions should be in the hands of those dedicated to their preservation, not to those who willfully plunder them for a 16th mansion in Miami Beach or to put another addition to their Montauk beach house.

I am pleased to be shop steward in The Newspaper Guild, which allows me to speak this truth to power, and I hope to still have my job after this.

But I’ve been shouting into the wilderness for some time about this and I’m really pleased that, with this legislation, Washington is finally beginning to look at what is a crucially important issue for this country.

Needless to say, I was not the only speaker. But Reynolds and I were the only two speakers addressing the journalism aspect of hedge fund ownership.

You can watch video of the entire press conference here if you have an hour to spare.

The majority of the speakers who were not members of Congress, were former workers of retail chains which have been particularly savaged by hedge funds, also called “private equity,” that, as Reynolds so succinctly put it, stripped them for parts.

Many of those chains you may know: Toys R Us; K-Mart; Payless Shoes (plundered and run into the ground and bankruptcy by the same hedge fund that owns The Mercury); Shopko; Burlington Coat Factory and even Caesar’s casino in Atlantic City.

They are part of United for Respect, a group organized and comprised of former workers who lost livelihoods, pensions and careers to feed hedge fund bottom lines. But rather than lose hope, they banded together to fight to make sure it doesn’t happen to others.

“Wall Street robbed me of what I took my entire life to build,” said Madelyn Garcia, who worked for a Florida Toys R Us for 30 years and, after promises of a generous severance package for staying to help close out the store, received one week’s pay.

“Consider local news to be a patient with a pretty serious chronic condition. Now give that patient flesh-eating bacteria. That’s the additional threat hedge fund ownership poses to the survival of the patient.”

Ruth Ann Joyce and her husband were among 2,100 workers who lost their jobs when Caesars Casino in Atlantic City was closed in 2014. She now works three jobs, including as a banquet bartender at Harrah’s. It took her husband, who suffered from depression because he felt he was not providing for his family, a year-and-a-half to find a new job.

These hedge funds are all about cutting cost, but the human cost never seems to count in the accountant’s ledger.

These workers also suffered from the same practices we’ve seen sinking newspapers: huge fees for managing a company they just bought; 20 percent shares skimmed off the top of company profits; and huge debt loads that burden the company they are supposed to be “saving,” but which the hedge funds have no responsibility for re-paying.

The members of Congress who introduced The Stop Wall Street Looting Act say it is designed to curb the worst of these abuses.

According to a press release from Warren’s office, the primary provisions of the bill include:

- Require Private Investment Funds to Have Skin in the Game. Firms will share responsibility for the liabilities of companies under their control including debt, legal judgments and pension-related obligations to better align the incentives of private equity firms and the companies they own. In order to encourage more responsible use of debt, the bill ends the tax subsidy for excessive leverage, and closes the carried interest loophole.

- End Looting of Portfolio Companies. To give portfolio companies a shot at success, the proposal bans dividends to investors for two years after a firm is acquired and ends the extraction of wealth from acquired companies through excessive fees.

- Protect Workers, Customers, and Communities. This proposal prevents private equity firms from walking away when a company fails and protects stakeholders by:

- Prioritizing worker pay in the bankruptcy process, and improving rules so workers are more likely to receive severance, pensions, and other payments they earned.

- Creating incentives for job retention so that workers can benefit from a company’s second chance.

- Ending the immunity of private equity firms from legal liability when their portfolio companies break the law, including the WARN Act. When workers at a plant are shortchanged or residents at a nursing home are hurt because private equity firms force portfolio companies to cut corners, the firm should be liable.

- Clarifying that gift cards are consumer deposits, ensuring their priority in bankruptcy.

- Empower Investors by Increasing Transparency. Private equity managers will be required to disclose fees, returns, and political expenditures so that investors can monitor their investments and shop around.

- Require Regulators to Address Risky Leverage. The Dodd-Frank provisions that require arrangers of corporate debt securitization to retain some of the risk will be reinstated.

“Our laws should reward hard work and persistence, not loopholes and financial looting,” said U.S. Rep. Ro Khanna, D-17th Dist. in California, who spoke Thursday and is co-sponsoring the bill in the House.

Instead, hedge funds “are shifting money around and getting paid millions of dollars for it,” he said. “Who do these paper shufflers think they are? Are they curing cancer? Founding a university? That’s not what built America.”

Hedge funds “take a company, suck the value out of that company, then walk away,” said Sen. Tammy Baldwin, D-Wisconsin, who is a co-sponsor of the bill and defended it later in the day on Fox News Business. “We need to rip up the predatory playbook Wall Street uses to leave workers with nothing but pink slips.”

“Wall Street leeches buy up struggling companies, saddle them with debt, pay themselves first, and then strip those companies for their parts,” said Sen. Sherrod Brown, D-Ohio. “It’s exactly what’s wrong with this country.”

“People who have worked hard their whole lives to earn a pension deserve to be able to rely on that money still being there when they retire,” said U.S. Rep. Rashida Tlaib, D-13th Dist. in Michigan.

“They do not deserve greedy Wall Street firms raiding their earnings and playing games with their futures,” said Tlaib. “We need to stand up for workers and communities in the face of toxic corporate greed and the Stop Wall Street Looting Act is a powerful tool in that fight.”

The bill’s chances of passage while Republicans control the Senate and the White House may seem slim. Ultimately, the voters may determine its chances.

But at least its introduction and what I hope will be the subsequent debate about its merits has brought the dangers hedge funds pose to workers and local news to a wider national audience.

And that’s something to shout about.

![]()